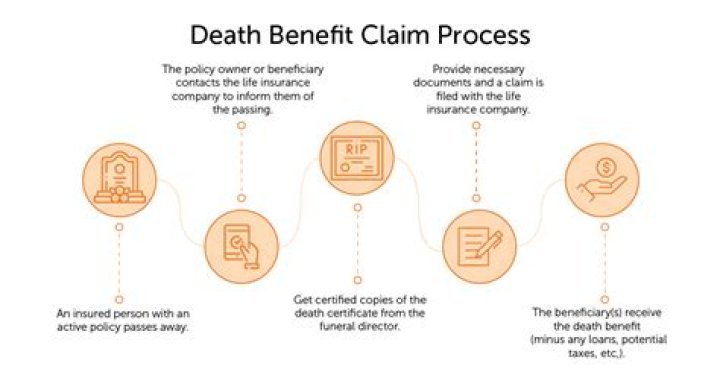

Can an insurance policy provide more than a death benefit?

Term life insurance guarantees payment of a stated death benefit to the insured’s beneficiaries if the insured person dies during a specified term. These policies have no value other than the guaranteed death benefit and feature no savings component as found in a whole life insurance product.

What factors influence insurance?

Below are the 15 rating factors most often used by car insurance companies, along with some associated costs by insurer.

- Age. Age is a very significant rating factor, especially for young drivers.

- Driving history.

- Credit score.

- Years of driving experience.

- Location.

- Gender.

- Insurance history.

- Annual mileage.

Is cash value included in death benefit?

The life insurance company will absorb the cash value and your beneficiary will be paid the policy’s death benefit. However, there is an exception. The beneficiary receives both the cash value and the face value if you purchased a policy rider that calls for that.

How can I add an additional insured to my insurance policy?

Whether you are the additional insured or you need to add one on your insurance policy, it is important to know how additional insured works. Make sure the additional insured is listed properly on your policy by checking your declaration page or asking your agent.

What are the benefits of an additional insured policy?

In addition to avoiding the problems associated with contractual liability coverage alone, additional insured status also has several other benefits to the insured concerning defense costs and subrogation. CGL policies provide unlimited, or uncapped, defense costs.

Do you have to be an additional insured on a PL policy?

Unfortunately, not all clients are well versed in insurance as it relates to de- sign and construction projects. Such clients may seek contract provisions that require their prime designers to name them as additional insureds on their professional liability (PL) policies.

Why does a contractor have to be additional insured?

The contractor lists the building owner as additional insured so that if there’s a loss that creates liability for the building owner, the contractor’s policy can be responsible for it. The problem is that additional insured and additional interest behave very differently in the event of a loss.