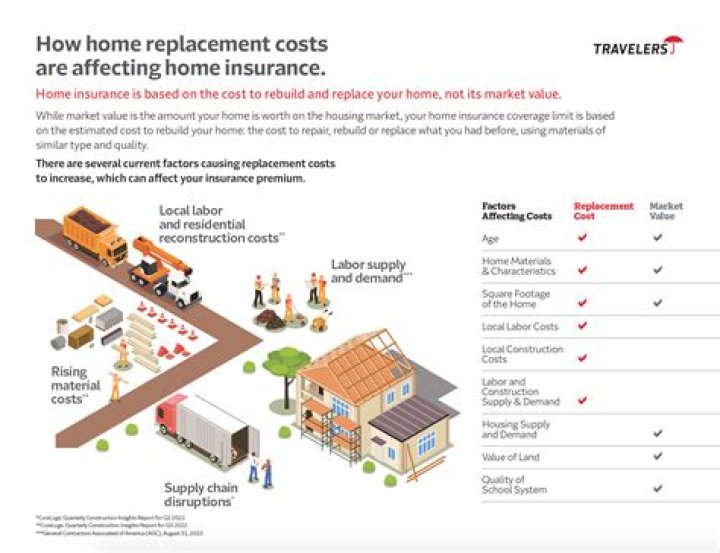

How do insurance companies determine replacement value of home?

Insurance companies will estimate your home replacement value based on costs of local labor, readily available materials, additions you may have built, age of the house, etc. To put it simply, they factor in anything that will affect how much your home will cost to rebuild.

What is not usually covered by homeowners insurance?

Termites and insect damage, bird or rodent damage, rust, rot, mold, and general wear and tear are not covered. Damage caused by smog or smoke from industrial or agricultural operations is also not covered. If something is poorly made or has a hidden defect, this is generally excluded and won’t be covered.

Does homeowners cover market value?

Some insurance companies will offer what is called a Market Value type of policy. It is also known as a “Functional Replacement Cost” or “Modified Loss Settlement”. Market Value is the amount a buyer would pay for a home, including the land regardless of how much it would cost to rebuild it.

How is home replacement cost calculated?

A simple way to get a replacement cost estimate for your home is to find the average per-foot rebuilding cost for your area and to multiply that by your home’s overall square footage. This information can usually be found on the websites of local construction companies or by reaching out to a contractor yourself.

Is replacement cost the market value?

Market value is the estimated price at which your property would be sold on the open market between a willing buyer and a willing seller under all conditions for a fair sale. Replacement cost is the estimated cost to construct, at current prices, a building with equal utility to the building being appraised.

Is rebuild cost more or less than market value?

The rebuild cost is the amount it would cost to completely rebuild your home if it was destroyed beyond repair. It includes the price of labour and materials. This cost is usually lower than your home’s sale price or market value.

How does home insurance work for replacement cost?

Most homeowners insurance policies come with replacement cost coverage for the structure of your home. Dwelling coverage typically helps pay to repair or rebuild your home using materials of a similar quality, says the III. It generally does not take into account depreciation of your home due to factors such as age.

How is replacement value determined in an insurance policy?

In this instance, the insurer allocates at the beginning of the policy a replacement value to the item. No matter how the item rises (or falls) in value in the interim – it is the fixed value replacement cost which is paid to the insured party in the event of a claim.

Is there loss of use coverage on homeowners insurance?

Yes, in most cases. Most standard homeowners policies include loss of use coverage, which can help pay expenses such as hotel bills and meals when you’re temporarily displaced from your home by a covered loss. But keep in mind that policy limits apply and your coverage will only pay for the additional costs you incur above your normal expenditures.

Do you have to replace items in a home insurance policy?

You must first replace the items before you’re able to collect the payment. But there are some exceptions. For example, in many high-value home policies, the terms may be different. Depending on the size of the loss and the type of claim, you’ll likely be asked to provide a list of items and their values.